Introduction

The fast development of mobile technologies has completely transformed financial transactions in recent years. The importance of safe and fast mobile financial transactions is growing as the globe gets more and more linked via mobile devices. There have been several problems with conventional, centralized banking systems, such as security breaches, manipulation of data, and transaction delays. The introduction of the technology known as blockchain, nonetheless, has presented fresh opportunities for strengthening the safety and dependability of mobile payments. In this article, Dissertation writing Service Birmingham and the pros and drawbacks of using blockchain to facilitate secured mobile money transfers are discussed.

Discussion

Independent and Unchangeable

It’s well aware of the need for decentralization and understands that blockchain is dispersed. Here, everyone who has a copy of the data agrees on a single version. This agreement ensures that data integrity is properly protected. One of the most remarkable things about blockchain technology is its immutability, which also reveals the most promising applications of smart contracts (Rathore et al., 2020). Increased trust and authenticity in the data may be achieved via this idea’s potential to reimagine the whole data audit process and help Essay writing service UK. Bitcoin is a peer-to-peer network that functions as a distributed ledger. The sole method to know for sure whether a transaction is successful is to check it out. This blockchain’s decentralized structure removes the need for middlemen like banks in the environment of “mobile financial transactions”, which in turn decreases transaction costs and increases transaction speed (Ali et al., 2020). Mobile monetary transactions are made more secure and transparent due to the permanent nature of blockchain data, which means that when a transaction has been tracked, it cannot be altered or messed with.

A game-changing answer to these difficulties, blockchain technology provides a more secure and private environment for conducting mobile monetary transactions.

Security via Cryptography

Blockchain’s powerful cryptography algorithms are the foundation of its security. Cryptographic algorithms protect the integrity of the blockchain and each transaction conducted on it, making the information unbackable and unreadable by any other party (Prabakaran and Ramachandran, 2022). Each transaction is given its own digital signature by use of these methods; if any tampering with the data is attempted, the network will identify it and reject the transaction as illegitimate.

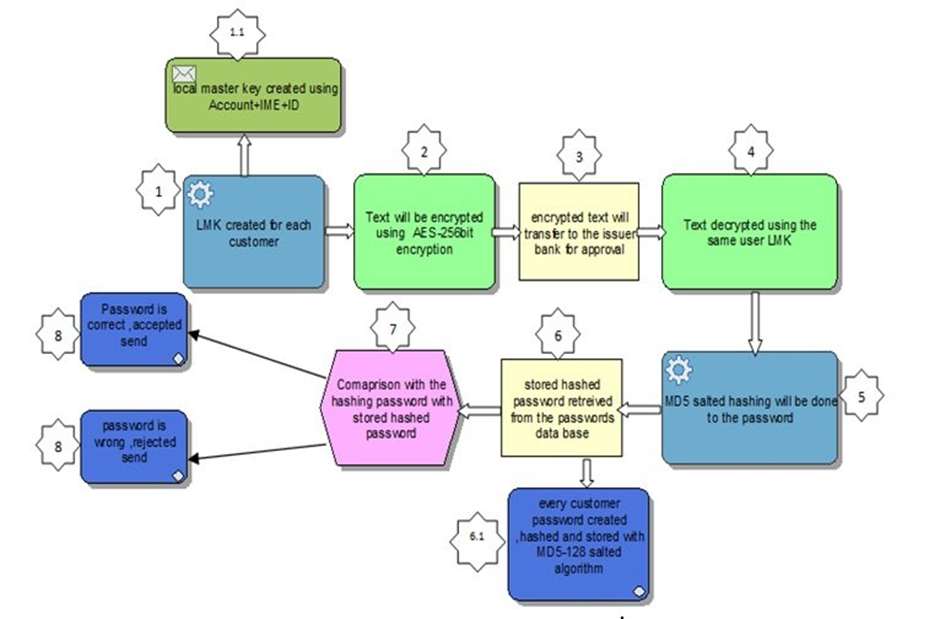

Figure 1: Mobile transaction process using blockchain

(Source: researchgate, 2021)

Dispersed Authority and Group Decision Making

Blockchain relies on a network of decentralized nodes for its operation. Different nodes in the network, rather than a centralized server, verify and record transactions. Each time a new batch of transactions is added to the blockchain, all of the nodes involved must reach an agreement on whether or not those transactions are legitimate (Andronie et al., 2021). Because of the decentralized nature of consensus, the transaction history can’t be altered by a single actor, making the system secure against hacking. As long as the network as a whole is secure, financial transactions conducted through mobile devices are protected from tampering.

Transparency and inalterability

Once a transaction has been added to the blockchain, it can no longer be changed or removed. This openness is especially important for Online Assignment help UK and mobile financial interactions since it lets consumers keep tabs on their payments and guarantees that money gets where it’s supposed to go without any interference from other parties.

Anonymity and Confidentiality

Users’ true names are not connected to their financial dealings; therefore, this pseudonymity safeguards their privacy. Even while Bitcoin transactions are visible to anybody, the encryption keys themselves are kept secret (Balapour et al., 2020). This option gives customers more say over their information and lessens the likelihood of private details getting into inappropriate hands.

Smart contracts

Smart contracts, which automatically carry out their terms when certain circumstances are met, are often supported by blockchain platforms. There is no space for mistake or manipulation in a smart contract since it is executed on its own when the predetermined circumstances are satisfied (Kurt Peker et al., 2020). The participants to a mobile cash transaction are more likely to abide by the conditions agreed upon since these contracts are clear, auditable, and permanent. Smart contracts further improve the safety and confidentiality of mobile banking transactions since they cannot be altered and must be followed by all parties.

Cross-border payments

In order to ease transactions between entities in various countries and utilize different currencies, blockchain computing is being used for cross-border payments.

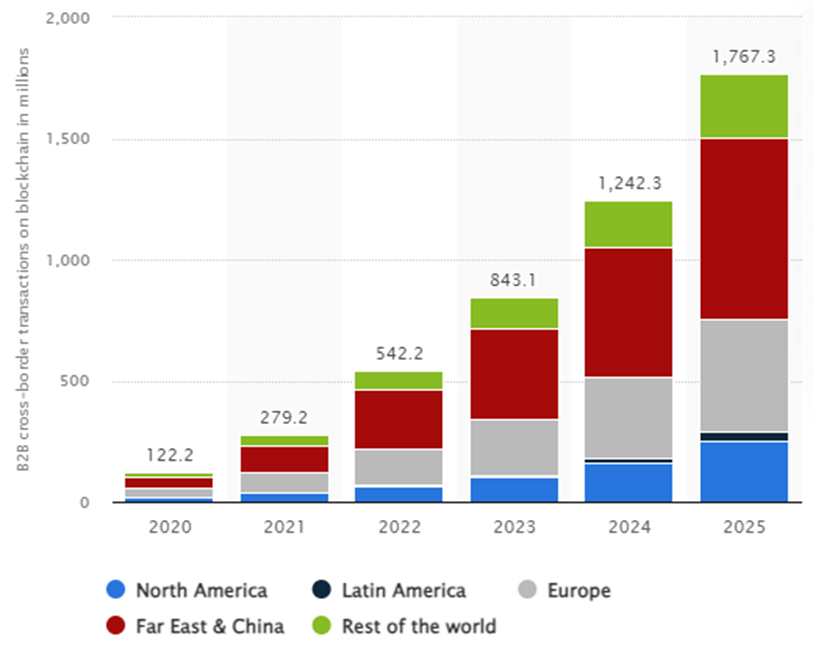

The International Money Transfer Market

By the year’s conclusion, international transactions will total US $156 trillion. By the end of 2022, B2B cross-border payments alone will amount to $35 trillion, as reported by Juniper Research. In addition, as technology advances, more and more international transactions are being conducted through distributed ledger systems. According to the World Bank, the typical cost of sending money abroad is roughly 7%, and the G20 has been working to bring that down to 5%. Governments in the North and South Americas, Asia, as well as Africa, are now the ones setting the standard for international money transfers.

Figure 2: B2B Cross-border transaction

(Source: statista, 2021)

The Conventional Method of International Funds Transfer

A banking network connects many worldwide communication networks that facilitate standard international financial transactions. A remittance or money transfer is an international wire transfer conducted by a business having connections to financial institutions like banks and credit unions (Wewege et al., 2020). The lack of uniformity in the ledger amongst the sender of the message and the recipient of a conventional international payment raises additional security concerns.

Global transactional changes made possible by blockchain technology

Blockchain transactions are starting to be tested by more traditional financial institutions. While the surface-level technology is the same, the underlying infrastructure has to be modified somewhat for it to function on the blockchain (Shaikh et al., 2022). Blockchain technology is already being progressively used by government organizations for the management of financial settlements, and the improvement of current legal frameworks, including the distribution of grants.

Challenges

The biggest problem is that the majority of individuals aren’t good with technology. There’s a lack of transparency in the cryptocurrency market’s governing structures. Financial technology behemoths like Wise and SWIFT are unwilling to use Bitcoin and distributed ledger systems at the present time (He et al., 2022). When a larger number of national central banks begin using blockchain for international transfers, then they will begin deploying related network infrastructure.

Energy efficiency

- In contrast to conventional databases, a blockchain does not make it possible for transactions or information to be modified after they have been recorded. To ensure that all participants in a network have access to an accurate and immutable history of all transactions, open ledgers are used. With a centralized database like this, businesses may avoid the time and effort waste that comes with maintaining several records of the same transaction.

- Blockchain enables decentralized cloud-based storage with virtual computers and distributed two-way communication between drivers plus parking lot proprietors. As a security measure, it provides assurance via open communication between drivers and parking lots (Razaque et al., 2022). By combining Blockchain and IoT, it may soon have a safe platform for motorists to use GPS navigation systems to plot the most efficient and quickest routes to parking garages.

- Virtualization is a key technology for optimising cloud server resources and services, creating a greener, more cost-effective setting for cutting-edge urban software.

- As a result, it encourages digital car rental in clever parking as a means of protecting individual privacy. Blockchain networks’ usage of energy is a problem as well, especially for coins like Bitcoin that use energy-intensive proof-of-work validation procedures (Yang and Masron, 2022). Mining uses a lot of energy, and this has led to ecological worries. Effective blockchain solutions may be on the horizon thanks to continued study and the investigation of alternative consensus methods like proof-of-stake.

Conclusion

It can be concluded that the world becoming increasingly interconnected via mobile devices, the need for quick and secure mobile banking transactions increases. Verifying a purchase is the only way of knowing for sure whether it went through. In the context of “mobile financial transactions,” the decentralized nature of this blockchain eliminates the need for intermediaries like banks, resulting in lower transaction costs and faster confirmation times. Integrating blockchain-enabled safe mobile payments is the key to a more accessible, efficient, and integrated financial ecosystem as the globe continues to take on the digital era. Acceptance of this technology in a responsible manner has the potential to significantly alter the future of finance, leading to a safer and more accessible international monetary system. Using these techniques, a unique digital signature is generated for each transaction; if an effort is made to tamper with the data, the network will recognize it and invalidate the transaction as fraudulent. Because mobile cash transactions are explicit, auditable, and irreversible, the parties involved are more likely to adhere by the terms agreed upon. Due to the immutability and binding nature of smart contracts, mobile banking transactions are even more secure and private.

Reference

Ali, G., Ally Dida, M. and Elikana Sam, A., 2020. Two-factor authentication scheme for mobile money: A review of threat models and countermeasures. Future Internet, 12(10), p.160. https://www.mdpi.com/1999-5903/12/10/160/pdf

Andronie, M., Lăzăroiu, G., Ștefănescu, R., Ionescu, L. and Cocoșatu, M., 2021. Neuromanagement decision-making and cognitive algorithmic processes in the technological adoption of mobile commerce apps. Oeconomia Copernicana, 12(4), pp.1033-1062. http://www.economic-research.pl/Journals/index.php/oc/article/download/1939/1871

Balapour, A., Nikkhah, H.R. and Sabherwal, R., 2020. Mobile application security: Role of perceived privacy as the predictor of security perceptions. International Journal of Information Management, 52, p.102063. https://www.academia.edu/download/62348644/Mobile_application_security_Role_of_perceived_privacy_as_the_predictor_of20200312-99096-yk445z.pdf

He, C., Milne, A. and Zachariadis, M., 2022. Central bank digital currencies and international payments. https://swiftinstitute.org/wp-content/uploads/2023/04/SWIFTInstitute_CBDCInternationalPayments_PublishedMay2022.pdf

Kurt Peker, Y., Rodriguez, X., Ericsson, J., Lee, S.J. and Perez, A.J., 2020. A cost analysis of internet of things sensor data storage on blockchain via smart contracts. Electronics, 9(2), p.244. https://www.mdpi.com/2079-9292/9/2/244/pdf

Prabakaran, D. and Ramachandran, S., 2022. Multi-factor authentication for secured financial transactions in cloud environment. CMC-Computers, Materials & Continua, 70(1), pp.1781-1798. https://pdfs.semanticscholar.org/8fc0/60ae61455be660ebfcc9a4bec1ac4ffdc7e2.pdf

Rathore, H., Mohamed, A. and Guizani, M., 2020. A survey of blockchain enabled cyber-physical systems. Sensors, 20(1), p.282. https://www.mdpi.com/1424-8220/20/1/282/pdf

Razaque, A., Jararweh, Y., Alotaibi, B., Alotaibi, M., Hariri, S. and Almiani, M., 2022. Energy-efficient and secure mobile fog-based cloud for the Internet of Things. Future Generation Computer Systems, 127, pp.1-13. https://www.researchgate.net/profile/Bandar-Alotaibi-4/publication/354177900_Energy-efficient_and_secure_mobile_fog-based_cloud_for_the_Internet_of_Things/links/6129fd0738818c2eaf64ad3e/Energy-efficient-and-secure-mobile-fog-based-cloud-for-the-Internet-of-Things.pdf

Shaikh, A.A., Alamoudi, H., Alharthi, M. and Glavee-Geo, R., 2022. Advances in mobile financial services: a review of the literature and future research directions. International Journal of Bank Marketing, 41(1), pp.1-33. https://www.emerald.com/insight/content/doi/10.1108/IJBM-06-2021-0230/full/pdf

Wewege, L., Lee, J. and Thomsett, M.C., 2020. Disruptions and digital banking trends. Journal of Applied Finance and Banking, 10(6), pp.15-56. https://www.researchgate.net/profile/Luigi-Wewege/publication/343050625_Disruptions_and_Digital_Banking_Trends/links/5f136f93a6fdcc3ed7153217/Disruptions-and-Digital-Banking-Trends.pdf

Yang, C. and Masron, T.A., 2022. Impact of digital finance on energy efficiency in the context of green sustainable development. Sustainability, 14(18), p.11250. https://www.mdpi.com/2071-1050/14/18/11250/pdf